Anteya Research

Earthquake and Natural Disaster Risk in Bali: How to Insure Against It (2026)

April 22, 2026

Across several thousand buyer conversations Anteya logged between 2023 and 2026, only a handful raised insurance or natural-disaster-risk questions directly. Low frequency: most foreign buyers process the risk question implicitly through property choice rather than through insurance. This article maps what actually can be insured against in Bali, what it costs, and when the expense is genuinely worth the coverage.

Anteya observation: Our Q1 2026 Bali primary-market dataset tracks several hundred projects across the main foreign-buyer sub-markets. Risk exposure varies materially by location: coastal Canggu, Seminyak, and low-lying parts of Sanur carry different exposure profiles than inland Ubud or clifftop Bukit properties.

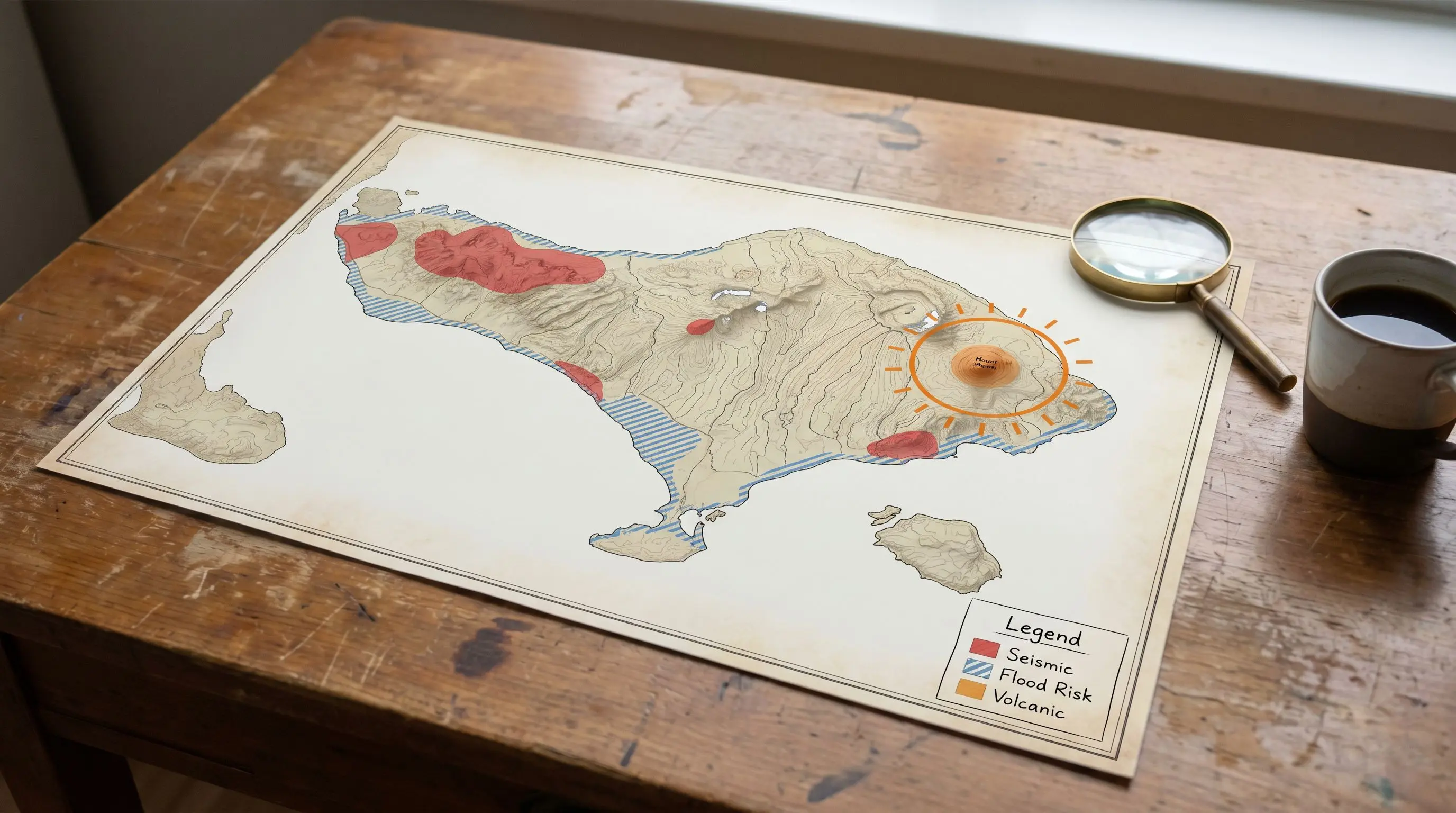

The risks foreign buyers actually face in Bali

Seismic / earthquake: Indonesia sits on the Pacific Ring of Fire, and Bali falls within Indonesia's moderate-seismicity zone (roughly zone 3-4 on the SNI hazard scale). Bali itself has had no catastrophic property-destruction event in recent decades; the nearest large regional event was the 2018 Lombok earthquake (magnitude 7.0), which caused limited damage in north Bali. Building code (SNI 1726) requires seismic-resistant structural design on new construction, and reputable developers comply. Measurable earthquakes do occur, but the protective layer (modern code + no recent catastrophic event) is the more relevant frame than the seismic-zone designation alone.

Tsunami: Coastal Bali carries low-but-non-zero tsunami risk, and exposure differs sharply by coastal profile: cliff coasts carry minimal tsunami exposure, while low-lying beach areas carry higher risk. The 2004 Aceh tsunami did not reach Bali. Potentially exposed flat-coast areas include the coastal Canggu beach strip (within 100-300m of beach), Sanur coastal strip, Nusa Dua beachfront, and Pererenan beachfront. Many Bali "beachfront" properties sit 20-50m above sea level due to cliff or dune geography, which reduces exposure materially, but flat coastal areas carry real risk.

Flood: Monsoon-season (October–April) flooding is a real operational issue in specific Canggu sub-markets: Berawa lower streets, parts of the Shortcut, Pererenan beachfront, low-lying Cemagi roads. Typically ankle-to-knee-deep, 1–4 hours duration, localised. Rarely catastrophic but disruptive to rental operations.

Fire: Normal residential fire risk. Electrical-origin fires are the predominant concern given variable PLN quality and non-standard electrical installations on older/cheaper construction.

Volcanic ash: Mount Agung's periodic activity can disrupt air travel (affecting the tourism cycle indirectly) but rarely damages Bali property directly; the volcano's flanks sit far from residential areas foreigners buy.

Civil unrest / political risk: Very low. Bali has been politically stable through Indonesia's modern history.

What property insurance is available in Bali

The Indonesian property-insurance market in Bali is specialised but functional, with several major carriers active; villa policies for foreign owners are typically arranged through a local broker. Coverage options commonly on offer:

- Fire insurance: baseline coverage. Available from most Indonesian general insurers (Allianz Indonesia, AXA Mandiri, Sinar Mas, Generali Indonesia, and others). Premium typically in the low-tenths of a percent of insured value per year for a standard villa.

- Earthquake extension: add-on rider to fire insurance. Adds a further small-fraction-of-a-percent annual premium. Available through major Indonesian insurers.

- All-risks property insurance: bundles fire, earthquake, windstorm, tsunami, vehicle impact, and water damage. Premium typically a few tenths of a percent of insured value per year. Offered by premium-tier insurers primarily to corporate buyers and higher-value individual policies.

- Content / contents insurance: separate from structure insurance. Covers furnishings, appliances, and soft goods, priced as a small percentage of declared contents value per year.

- Liability insurance: covers guest-injury claims arising from rental operation. Effectively required for STR operators; pricing for a standard villa is in the low-hundreds to high-hundreds of dollars per year.

- Business-interruption insurance: covers lost rental revenue during repair periods after insured events. Priced as a small percentage of projected annual revenue.

Exact premiums vary widely by carrier, policy structure, location, and construction type. Confirm quotes with a licensed Indonesian broker.

What to actually buy

A practical stack for a mid-sized villa operating as a rental:

- Baseline: all-risks property insurance on structure (fire + earthquake + windstorm + tsunami + water).

- Contents: separate contents policy for furnishings and appliances.

- Liability: STR guest-injury coverage.

- Business-interruption (optional): if rental revenue is the primary investment thesis.

For an owner-occupied (non-rental) villa, liability and business-interruption can be dropped, which cuts annual cost materially. Get side-by-side quotes from at least two carriers; spreads are wide on identical specs.

"Are these villas completed or off-plan, and if off-plan, what buyer protections are in place?"

Buyer inquiry, Anteya CRM, 2025

During the construction phase, contractor-side insurance (CAR, Contractor's All Risks) is the relevant coverage, held by the developer. After handover, ownership of the property's insurance obligation transfers to the buyer. This transition is often a coverage-gap moment worth specifically planning for.

"We went in family vacation for the first time in the end of June 2026."

Buyer inquiry, Anteya CRM, 2026

That family-vacation introduction to Bali usually happens in dry season (June sits mid-dry-season). Many buyers never experience the November–April monsoon before purchasing. Most buyers first see Bali in dry season; flood coverage is the line item that protects you against the monsoon-season reality you didn't see.

What insurance does NOT cover

Standard exclusions in Indonesian property policies:

- War and terrorism: typically excluded; optional endorsements available.

- Nuclear / radioactive: excluded (not a Bali-relevant risk).

- Pre-existing damage or defect: policy covers new events, not rectification of known issues.

- Mould and gradual deterioration: generally excluded despite tropical-climate relevance.

- Banjar / desa adat disputes: not an insurable event.

- Developer default / PPJB non-performance: not covered by property insurance; this is a PPJB-structure question, not an insurance question.

Sub-market-specific risk profile

Risk-and-coverage profiles vary sharply by sub-market. Clifftop Melasti product faces minimal tsunami exposure and is typically built to current seismic standards. Low-lying coastal Pererenan carries moderate monsoon-flood exposure. Nusa Dua beachfront sits on elevated terrain with an established insurance market around it. The underwriting question is always location-specific before it's product-specific.

"Could you please let me know if the property you are looking for is for leisure or to maximize ROI?"

Buyer inquiry, Anteya CRM, 2025

The insurance-buying calculus differs between leisure and ROI-driven ownership. Leisure owners typically under-insure (single annual premium feels like pure cost); ROI-driven owners treat insurance as an operating-expense line that protects revenue continuity. ROI-driven owners buy business-interruption coverage that leisure owners typically skip.

FAQ

Do I need property insurance in Bali?

Not legally required for residential ownership in Indonesia, but strongly recommended. Fire-only cover is inexpensive relative to structure value. For rental-operating properties, liability insurance is essentially required: one guest-injury claim can exceed decades of premium.

How much does Bali property insurance cost?

Premiums are quoted as a small percentage of insured value per year, with fire-only at the low end and all-risks (fire + earthquake + windstorm + water) a few tenths of a percent higher. Add separate line items for STR liability, contents, and optional business-interruption cover. The market is thin enough that spreads between carriers on identical specs are wide; get at least two quotes from a licensed Indonesian broker.

Is Bali in an earthquake zone?

Yes. Indonesia sits on the Pacific Ring of Fire, and Bali falls within a moderate-seismicity zone. Bali experiences measurable seismic activity but has not had a catastrophic property-destruction event in recent decades; the nearest large regional event was the 2018 Lombok earthquake (M7.0). Indonesian building code SNI 1726 requires seismic-resistant design on new construction, and reputable developers comply. Earthquake-rider insurance is inexpensive and widely available.

What about tsunami risk in Bali?

Low-but-non-zero. Coastal strip exposure varies sharply by geography. Clifftop Bukit (Uluwatu, Melasti, Pandawa, Balangan): minimal exposure due to elevation. Flat coastal Canggu, Sanur, Nusa Dua beachfront: real though low-probability exposure. Most all-risks policies include tsunami in the covered-perils list.

Does insurance cover monsoon flooding?

Typically yes under all-risks policies; often excluded from basic fire-only policies. Monsoon-season flooding on specific low-lying Canggu streets (Berawa, Shortcut, Pererenan beachfront) is a real and recurring issue worth specifically confirming coverage for if buying in those sub-markets.

What's CAR insurance and who pays for it?

CAR (Contractor's All Risks) is construction-phase insurance held by the developer, not the buyer. It covers damage to the works during construction. After handover, coverage responsibility transfers to the buyer; make sure there's no gap between CAR expiry and the buyer's policy effective date. The notaris can help sequence this.

Is business-interruption insurance worth it for STR operations?

For seriously-operated rental villas: usually yes. Business-interruption coverage pays lost rental revenue during repair periods after insured events. Priced as a small percentage of projected annual revenue, it's a modest line item against protection of the primary revenue stream for the weeks or months a property can sit out of service during post-event repair.

Anteya Research is the editorial function of Anteya Real Estate, a Bali-based investment property advisory.

Browse Bali projects → Contact Anteya →

This article is general information, not insurance advice. Insurance products and coverage terms change; consult a licensed Indonesian insurance broker for your specific situation.